How to Read the SpaceX S-1: Not as an IPO Filing, but as an Infrastructure Map

By David Gassier — May 20, 2026 — 18 min read

On May 20, 2026, Space Exploration Technologies Corp. filed Form S-1 with the U.S. Securities and Exchange Commission (file number 333-296070, accession 0001628280-26-036936). The document is 226 megabytes of registration material and is now public on EDGAR. The price range and share count are still blank — those will arrive with the pricing amendment (S-1/A) later in the road-show. What is not blank is the operating data, the segment financials, the executive compensation tables, the capital structure, and the risk factors. The infrastructure story is fully disclosed.

Most analysts will read this filing for the valuation. They will skim the prospectus summary, jump to the financials, and write 800 words about Starlink revenue growth and dual-class shares. That reading is not wrong. It is incomplete.

This article reads the S-1 as what it actually is: a public declaration of integrated industrial infrastructure, in legally mandated detail, by a company that has chosen to disclose the geometry of its competitive moat. Every number cited below is taken from the filing itself. The article quotes the document directly where the language matters.

This is the third article in a sequence. Article 1 argued that Colossus is not a data center story — it is an execution velocity story. Article 2 showed that Starship and Colossus apply the same capability to different domains. This article confirms both theses with primary source citations.

1. What the S-1 Actually Discloses

The filing has a structure analysts will recognize: Prospectus Summary, Risk Factors, MD&A, Business, Management, Executive Compensation, Capital Stock, Financial Statements. What is unusual is the content in each section.

The Prospectus Summary on page 2 frames the company in three layers: Space, Connectivity, AI. It then immediately states the strategic claim that drives everything else:

"We are the only company building the integrated hardware and software infrastructure of the future across space, connectivity, and AI."

That is not a marketing line. It is a thesis statement that the rest of the 700+ pages defends with numbers. The disclosed financial segments map directly to these three layers. The risk factors are organized around their interdependencies. The pay package vests on milestones inside them. The capital structure protects the institutional capacity to execute them.

Three structural facts the S-1 establishes in the first 20 pages:

- xAI was acquired by SpaceX in early 2026. Specifically, the xAI Merger closed on February 2, 2026, and xAI is now disclosed as the AI segment of SpaceX. This is no longer a parallel company. It is a consolidated business line.

- The Anthropic Cloud Services Agreement is real and enormous. Anthropic has agreed to pay $1.25 billion per month through May 2029 for access to compute on COLOSSUS and COLOSSUS II. That is a $45 billion commitment over roughly three years from a single customer.

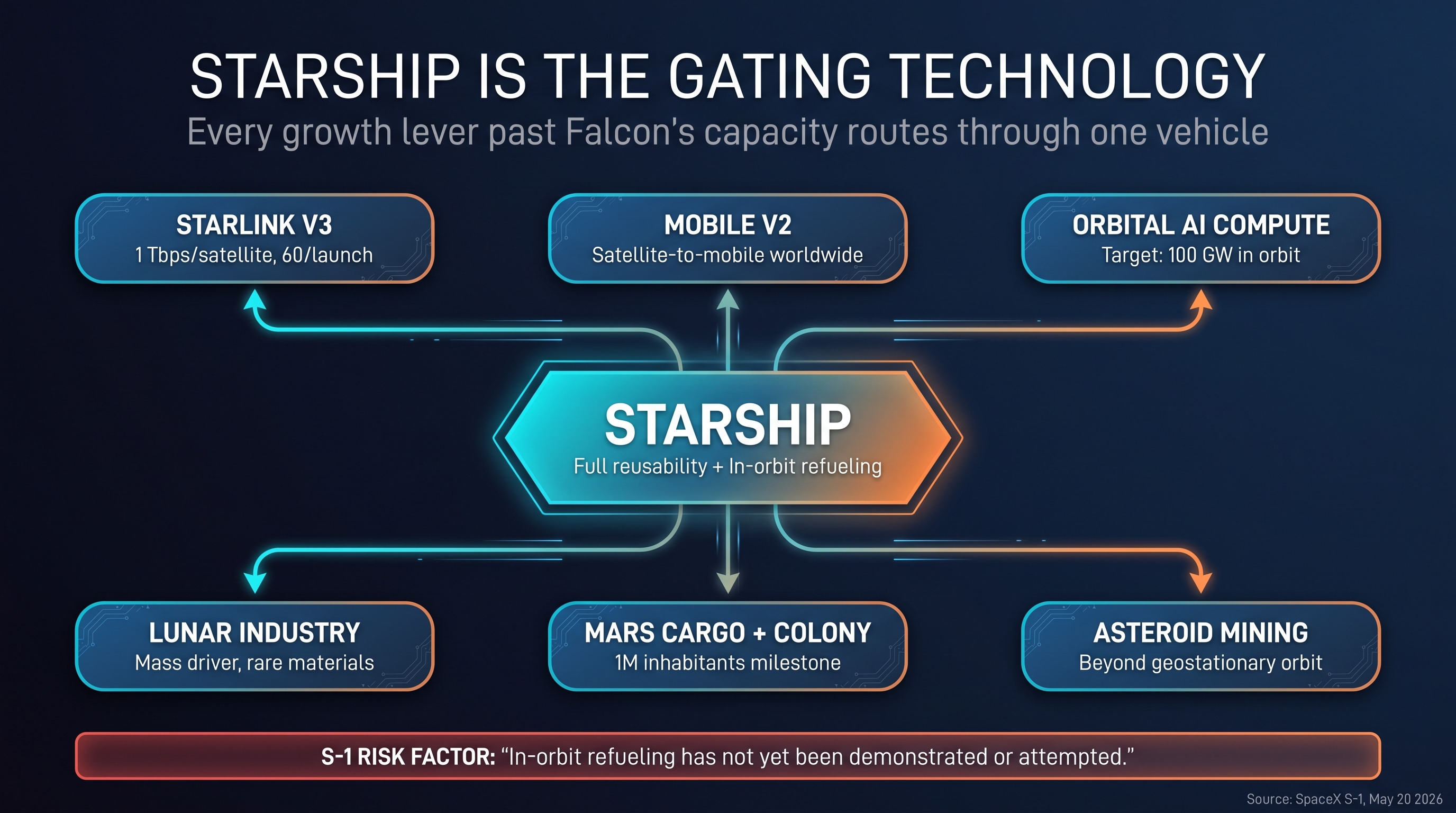

- Starship is the binding constraint on every growth lever. The S-1 states plainly that Falcon 9 and Falcon Heavy "are not capable of deploying V3 satellites and V2 Mobile satellites" and that "AI compute satellites at scale need full Starship reusability to be economically compelling." Starship is not one program among many. It is the gating technology for the entire growth strategy.

Everything that follows is the documentation of these three facts.

2. The Numbers That Actually Matter

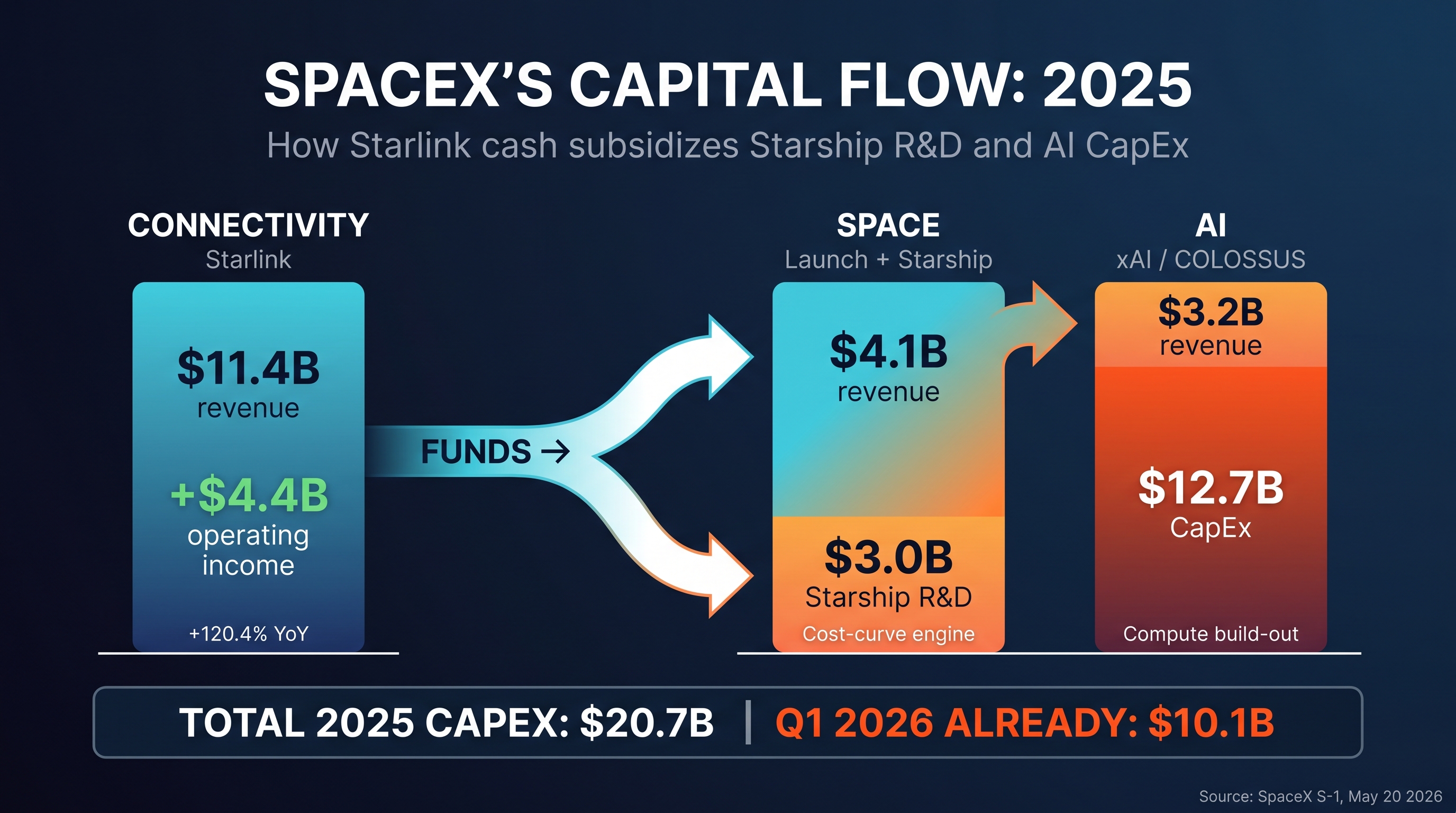

The S-1's segment disclosure is the most important table in the filing. Most readers will see consolidated revenue ($18.67 billion in 2025) and stop. The segment-level data is where the infrastructure thesis lives.

| Segment | 2025 Revenue | 2025 Op Income | 2025 CapEx | Q1 2026 Revenue | Q1 2026 CapEx |

|---|---|---|---|---|---|

| Connectivity (Starlink) | $11,387M | +$4,423M (+120.4% YoY) | $4,178M | $3,257M | $1,332M |

| Space (Launch + Starship) | $4,086M | $(657)M | $3,832M | $619M | $1,052M |

| AI (xAI / Colossus) | $3,201M | $(6,355)M | $12,727M | $818M | $7,723M |

| Consolidated | $18,674M | $(2,589)M | $20,737M | $4,694M | $10,107M |

Source: SpaceX Form S-1, prospectus summary, p. 4–5.

Read this table carefully. Three observations:

Connectivity is already a profitable, scaled telecom. Starlink delivered $4.4 billion in operating income in 2025, growing 120% year over year on top of 50% revenue growth. The operating leverage is kicking in. This is not a venture-backed business hoping to reach scale. It is a vertically integrated satellite ISP with positive unit economics and aggressive density compounding.

Space (the launch business) runs at near-breakeven before the Starship R&D charge. The S-1 separately discloses that Space funded $3.0 billion in R&D for Starship in 2025 alone, with another $930 million in Q1 2026. Net of that R&D, the launch business is profitable. The headline loss in the Space segment is almost entirely the cost of building the next vehicle.

AI is intentionally loss-making at scale. $12.7 billion of CapEx in 2025 and $7.7 billion in Q1 2026 alone. The AI segment is consuming capital faster than every other segment combined. This is not a typo or a one-time event. It is the cost of building gigawatt-class training clusters, and it is accelerating, not slowing.

The reading: SpaceX is using Starlink cash flow to fund Starship development, and using both to underwrite AI infrastructure expansion at a rate no public company has ever attempted. The S-1 makes this strategy explicit by disclosing the segment-level capital flow.

3. Starlink: Density Economics, Confirmed

The S-1 confirms what previously had to be estimated. As of March 31, 2026:

- 9,600 broadband satellites and approximately 650 V1 Mobile satellites in Low-Earth Orbit

- These constitute approximately 75% of all active maneuverable satellites in orbit

- 10.3 million Starlink subscribers across 164 countries, territories, and markets

- 7.4 million monthly unique devices using satellite-to-mobile services across 30 countries

- Median residential download speed of 225 Mbps during peak hours

Source: S-1, prospectus summary, pp. 3, 6.

These numbers are operational, but the strategic statement is the network share. Three-quarters of all active maneuverable satellites in orbit are SpaceX assets. That is not market leadership in the conventional sense. It is structural control of a finite resource — useful orbital slots and active spectrum — that competitors would need to physically displace to enter.

The S-1 also discloses the unit economics implicitly through segment margins. Connectivity generated $7.17 billion in Adjusted EBITDA on $11.39 billion in revenue in 2025 — a 63% Adjusted EBITDA margin. For comparison, mature terrestrial telcos run 35–45% EBITDA margins. Starlink is operating at margins closer to a hyperscale cloud business than a satellite ISP.

The forward signal is in the V3 disclosure. SpaceX expects to begin deploying next-generation V3 satellites in the second half of 2026, "designed to offer one Tbps of downlink capacity per satellite," using Starship to deploy "up to 60 V3 satellites" per launch — what the filing describes as "a potential twenty-fold increase in Starlink downlink capacity deployed relative to a Falcon 9 launch."

A 20× deployment multiplier on a constellation that already represents 75% of operational maneuverable satellites is what the financial models cannot yet price. It is also why the next section matters more than any other.

4. Starship Is the Gating Technology, and the S-1 Says So in Writing

The Risk Factors section is normally the place where companies bury their problems in boilerplate. SpaceX's S-1 does the opposite. Risk Factor #1 — the very first risk listed — is titled:

"Any failure or delay in the development of Starship at scale or in achieving the required launch cadence, reusability and capabilities thereafter would delay or limit our ability to execute our growth strategy."

The S-1 then explicitly states:

"Our current operational rockets, including Falcon 9 and Falcon Heavy, are not capable of deploying V3 satellites and V2 Mobile satellites."

"AI compute satellites at scale need full Starship reusability to be economically compelling."

These two sentences, read together, define the entire forward operating thesis. Three growth levers — Starlink V3, satellite-to-mobile V2, and orbital AI compute — all depend on Starship reaching full reusability and rapid turnaround. Falcon cannot substitute. There is no parallel program. The S-1 commits the company to this in legally binding disclosure.

The filing also confirms the operational status as of March 31, 2026:

- 11 Starship flight tests completed, with a 12th scheduled to debut "the next generation Starship vehicle and Super Heavy booster, powered by the next evolution of our Raptor engine and launching from a newly designed pad at Starbase"

- Starship V3 designed to deliver 100 metric tons to LEO in fully reusable configuration

- Falcon 9 has demonstrated a 34-flight reuse record for first-stage boosters

- The S-1 cites NASA estimates that Falcon 9 reduced launch cost from ~$18,500 per kilogram (historical industry average) to ~$2,700 per kilogram, with Starship targeting "99% or more" reduction below the historical baseline

The reading: Starship is not a research project. It is a disclosed corporate dependency. The 2025 spend of $3.0 billion in R&D and an additional $930 million in Q1 2026 R&D is what it costs to remove the gating constraint. The board is publicly accountable for delivering it.

A regulatory note buried in the same section deserves attention. Current FAA regulations "do not permit return-to-launch-site reentries for Starship, requiring us to obtain a waiver from the FAA, which is not guaranteed." The "chopstick" tower-catch architecture that enables rapid Starship reuse cannot legally operate without that waiver. The S-1 discloses this as a risk because it materially gates the cost-curve story.

5. The Anthropic Contract Is the AI Segment's Validation

For most of 2025, the question about the xAI / Colossus story was whether the infrastructure could be monetized to anyone outside the SpaceX/xAI internal stack. The S-1 answers that question.

"In May 2026, we entered into Cloud Services Agreements with Anthropic PBC ('Anthropic'), an AI research and development public benefit corporation, with respect to access to compute capacity across COLOSSUS and COLOSSUS II. Pursuant to these agreements, the customer has agreed to pay us $1.25 billion per month through May 2029, with capacity ramping in May and June 2026 at a reduced fee."

Source: S-1, pp. 24, 56 (multiple disclosure locations).

Let the number sit. $1.25 billion per month. Through May 2029. That is approximately $45 billion in committed contractual revenue from a single customer over roughly three years. Either party can terminate on 90 days' notice — which is standard cloud-services language and does not negate the disclosure value.

For context: the AI segment generated $3.2 billion in revenue in all of 2025. The Anthropic contract alone, once fully ramped, is $15 billion per year. That implies AI segment revenue scaling roughly five-fold from a single customer line by 2027, assuming no other contracts are signed.

But the strategic disclosure is not the revenue. It is the validation of the compute marketplace thesis. SpaceX is not just consuming COLOSSUS for Grok training. It is renting unused capacity to a competitor frontier lab. That is the same business model as AWS or Azure, applied to a vertically integrated AI training stack that the buyer cannot replicate.

Anthropic could have used any cloud. They picked the one that owns its own compute infrastructure, its own connectivity backbone, and its own launch capacity. The S-1 documents the consequence: the integrated stack is now a revenue-generating asset for third parties, not just a cost center for the operator.

6. The $28.5 Trillion TAM and the "Only Company" Framing

The most underreported single number in the S-1 is the total addressable market figure. The filing states plainly:

"We believe we have identified the largest actionable total addressable market ('TAM') in human history. We estimate that our quantifiable TAM is $28.5 trillion."

Source: S-1, prospectus summary, p. 11.

The breakdown, also from the filing:

- Space: $370 billion — space-enabled solutions (launch services, satellites, defense)

- Connectivity: $1.6 trillion — $870 billion Starlink Broadband + $740 billion Starlink Mobile + enterprise/government

- AI: $26.5 trillion — $2.4 trillion infrastructure + $760 billion consumer subscriptions + $600 billion digital advertising + $22.7 trillion enterprise applications

These estimates explicitly exclude China and Russia. The AI line dominates because the S-1 takes the position that AI is not a product category — it is a substitute for a meaningful share of the global enterprise software, services, and labor markets. Whether the $22.7 trillion enterprise applications figure is accurate is debatable. What is not debatable is that the company has filed it with the SEC as the basis for its growth plan.

Future Markets the S-1 names by name

Embedded in the same section is a list of markets that do not exist commercially today but that the company commits to pursuing. Quoting the filing directly:

"Future Markets: Point-to-point terrestrial travel · Space tourism · In-orbit manufacturing · Passenger and cargo transport to the Moon and Mars · Energy production on the Moon and Mars · Manufacturing capabilities on the Moon and Mars · Asteroid mining."

Source: S-1, prospectus summary, p. 11.

This is unusual disclosure. Most S-1s describe TAM in cautious legal language and reference only existing markets. SpaceX explicitly enumerates asteroid mining, lunar manufacturing, and interplanetary cargo transport as future markets the registration statement intends to address. The filing then concedes: "These industries do not exist today. While we believe these industries will develop over time, the manner in which they emerge, including the timing of commercialization, the scale and pace of adoption, and the applicable competitive, technical, regulatory, geopolitical factors are uncertain."

Lunar resources as a disclosed commercial thesis

The Business section goes further on the Moon specifically:

"Once resource utilization capabilities are proven feasible, we believe there is an opportunity to commercialize the harvesting and exportation of rare materials, which is estimated to be present on the Moon in quantities exceeding one million tons and has potential applications in future nuclear energy and quantum computing systems."

Source: S-1, business section, p. 166.

The S-1 also introduces the "lunar mass driver" — formally defined as "a launch system that we intend to build on the Moon's surface that will be designed to use electromagnetic acceleration to propel payloads into space without the use of rockets." This is not theoretical infrastructure planning. It is the architectural basis for lunar export economics — moving materials off the Moon at zero rocket-propellant cost.

Starship is the gating dependency for all of it

The S-1 leaves no ambiguity about how these markets become accessible:

"In-orbit refueling of Starship is essential to our lunar, Mars, asteroid mining, and other deep space ambitions beyond geostationary Earth orbit. In-orbit refueling is complex, and we have not yet demonstrated or attempted it."

Source: S-1, Risk Factors, p. 42.

This sentence does the heavy lifting. Every market past geostationary orbit — lunar industry, Mars cargo, asteroid mining, deep space science — is technologically downstream of Starship achieving in-orbit refueling, which has not yet been demonstrated. The 11 Starship flight tests completed as of March 31, 2026, do not yet include cryogenic propellant transfer in microgravity. That is the next gating capability.

"Only company" — used four times in the S-1

The filing uses the phrase "only company" deliberately, in four distinct contexts:

- Integrated stack: "SpaceX is the only company building the integrated hardware and software infrastructure of the future across space, connectivity, and AI."

- Launch: "SpaceX is the only company that has cracked the code on accessing space at scale."

- Orbital AI compute: "We believe orbital AI compute is an incredibly difficult technical challenge that only we can solve at scale in the near term. We are the only company that has already accomplished the key technical challenges associated with evolving connectivity satellites into AI compute satellites."

- Satellite manufacturing: "We believe SpaceX will be the first and only company to manufacture satellites at the scale of automotive manufacturing."

Blue Origin, ULA, Rocket Lab, and Amazon's Kuiper do not appear in the S-1 as integrated-vision competitors. They are mentioned only in industry data citations or not at all. The filing does not concede competitive parity at any layer of the integrated stack. Whether that posture is accurate or aggressive is a question for the market. The filing's position is unambiguous.

What COLOSSUS II is being used for right now

The S-1 confirms COLOSSUS II is operational and discloses two current uses: training Grok 5 (the next frontier model) and serving the Anthropic compute contract that ramps over May–June 2026.

A third use is disclosed less prominently — a product called "Macrohard", formally defined in the S-1 as "a platform we are currently developing that is designed to emulate digital workflows, augment human operation of computers, and create a fully AI-operated software company." If that description is accurate, Macrohard is an internal AI-operated enterprise software platform — the kind of system that would let a small team of engineers operate at the velocity of a much larger functional organization. It is the operational complement to Grok: where Grok is the consumer-facing frontier model, Macrohard is the internal productivity multiplier.

The S-1 does not explicitly disclose a Mars-planning unit using max-context Grok for terraforming and deployment strategy modeling. That said, the existence of such a team is the most reasonable inference from a $7.5 trillion market-cap pay package whose vesting depends on establishing a million-person Mars colony. A company that has booked Mars colonization as a fiduciary obligation has, by necessity, organized to plan it. The S-1 does not name the team. The compensation structure implies it.

7. Governance: The S-1 Codifies Founder Control More Tightly Than Meta, Google, or Snap

The Description of Capital Stock section (S-1, pp. 251–253) discloses a three-class structure that is more founder-controlled than any precedent in U.S. public markets.

- Class A common stock — offered to the public, 1 vote per share

- Class B common stock — held by Musk, 10 votes per share

- Class C common stock — employee equity, zero voting rights

A 10-to-1 supervoting structure is not new. Meta, Google, and Snap have similar mechanics. What is new is what comes next:

"Holders of our Class B common stock, voting separately as a class, are entitled to elect 51% of the total number of authorized directors (rounded up to the nearest whole number)."

This is not a voting-power calculation. It is a structural board carve-out. Even if Class A and Class C combined held more aggregate votes than Class B, Class B still elects a majority of the board outright. The supervoting math does not need to favor Musk for board control to remain with him.

The S-1 further discloses:

"Removal of Mr. Musk from his board and leadership roles (Chief Executive Officer and Chairman of our board) requires the approval of the holders of at least a majority of the voting power of the outstanding shares of Class B common stock, voting separately as a class."

In plain English: removing Musk requires Musk's approval. The S-1 codifies this in the charter.

Two additional structural provisions extend the founder-control architecture:

- Future Class B shares can only be issued to Musk, his family, or "permitted entities" defined in the charter. Dilution of the supervoting class is structurally impossible without changing the charter, which itself requires Class B class-vote approval.

- The company is incorporated in Texas, subject to TBOC anti-takeover provisions (Section 21.606), which add additional friction to hostile combinations beyond the supervoting mechanics.

The reading: institutional investors entering at IPO are not buying governance influence. They are buying access to the operational compounding of an institution whose decisions will be made by its founder for the foreseeable future. The S-1 is honest about this. Whether the discount appropriate to that risk is correctly priced is a different question.

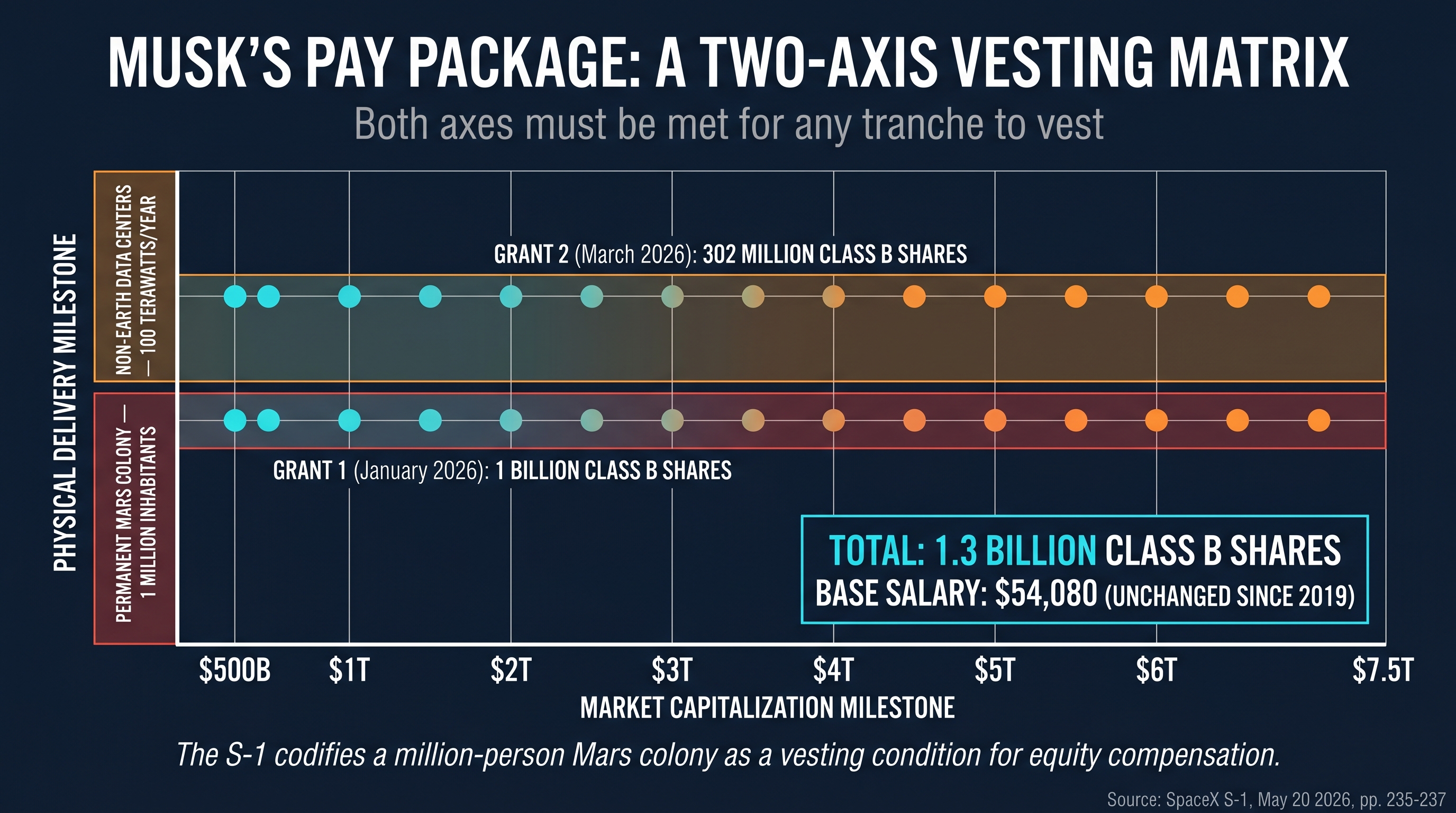

8. Musk's Pay Package Vests on Mars Colony and Orbital Data Centers

The Executive Compensation section (S-1, pp. 233–242) is where the integration of physical milestones into financial compensation becomes legally documented. Musk's base salary is $54,080, unchanged since 2019 and originally tied to California's minimum exempt-employee salary before the company's 2024 relocation to Texas. Almost all of his compensation is equity, structured as performance-based restricted shares of Class B common stock.

There are two grants disclosed.

Grant 1: One billion restricted shares, January 13, 2026

Vesting requires both conditions to be met for each tranche:

- The company achieving a specified market capitalization milestone, across 15 equal tranches from $500 billion to $7.5 trillion in $500 billion increments

- The Company's establishment of a permanent human colony on Mars with at least one million inhabitants

Source: S-1, pp. 235–236.

Read that again. The S-1 codifies a Mars colony of one million people as a vesting condition for equity compensation. This is not a press release. It is a disclosed obligation in a registration statement filed with the SEC. The board can be sued for inaccurate disclosure if the company materially deviates from pursuing this stated objective.

Grant 2: 302,072,285 restricted shares, March 23, 2026

This grant replaced an earlier xAI-issued performance award after the xAI Merger. Vesting requires both:

- Market capitalization milestones across 12 equal tranches from $1.065 trillion to $6.565 trillion in $500 billion increments

- "The Company's completion of non-Earth-based data centers capable of delivering 100 terawatts of compute per year"

Source: S-1, pp. 236–237.

Two observations on these grants:

The financial structure is unprecedented. Combined, Musk could receive over 1.3 billion additional Class B shares against achievements totaling roughly $7.5 trillion in market cap, conditional on physical infrastructure delivery on Mars and in orbit. The market-cap milestones alone are extraordinary. The physical-milestone overlay makes this the first executive compensation package in public-market history that vests on planetary-scale industrial deliverables.

The S-1 thereby commits the company to those deliverables in legally binding documentation. Mars colonization and orbital AI data centers are not aspirational. They are corporate obligations encoded into the compensation structure of the CEO. A board that abandons these objectives invites contract litigation. The architecture is self-reinforcing: governance keeps Musk in control, pay keeps the long-horizon objectives institutional, capital structure keeps the founder-class shares concentrated.

9. The Risk Factors Most Readers Will Skip

The Risk Factors section runs 38 pages. The risks that matter most for the infrastructure thesis are concentrated in the first 10 pages. Five deserve specific attention:

Starship dependency, restated. The S-1 is unambiguous: "Our ability to execute our growth strategy is highly dependent on Starship." Failure to achieve full reusability does not just delay one program — it cascades through Starlink V3, mobile V2, and orbital AI compute simultaneously.

FAA regulatory tolerance. Beyond the return-to-launch-site waiver, the S-1 notes that "the FAA's resources may become strained" with growing industry launch cadence, and that following anomalies "the FAA or other authorities may require investigations, impose corrective actions, or restrict or delay our ability to conduct launch operations." Regulatory friction is disclosed as a function of SpaceX's own pace.

Spectrum dependency on EchoStar deal. The S-1 discloses that the EchoStar AWS-4 and H-block spectrum acquisition, "approved by the FCC on May 12, 2026," is "subject to other closing conditions" and "expected to close in November 2027." Starlink V2 satellite-to-mobile services worldwide are conditional on this transaction completing and on subsequent international authorizations. The disclosure is honest that "there can be no assurance that these conditions will be satisfied."

AI segment regulatory exposure. The filing explicitly lists active investigations:

"We are subject to investigations and inquiries from regulators and law enforcement authorities in the United States and internationally concerning allegations that our AI products were used to create nonconsensual explicit images or content representing children in sexualized contexts, and similar matters."

It further discloses the Irish Data Protection Commission's February 2026 large-scale inquiry into xAI's GDPR compliance, the EU AI Act, California's Frontier Artificial Intelligence Act, and New York's Responsible AI Safety and Education Act. The S-1 acknowledges that AI product features such as Grok's "Spicy" Imagine Mode and "Unhinged" Voice Mode "present heightened risks" including potential market-access loss "which has occurred in the past."

CapEx ahead of revenue. Q1 2026 capital expenditures were $10.1 billion against $4.7 billion in revenue. The S-1 acknowledges that the company "may need to return to capital markets if the gap persists." This is the cost of building the infrastructure. It is also a financing dependency that requires market access to remain open during the build-out.

10. The Operator's Takeaway

The SpaceX S-1 is not a financial document. It is an industrialization playbook rendered in GAAP.

The instinct of most analysts will be to model Starlink revenue, apply a multiple, discount Starship, debate the AI losses, and arrive at a valuation range. That exercise has its place, but it misreads the document.

The S-1 confirms four things that change how we should think about software-platform investing more broadly:

- Compounding software value requires compounding physical substrate. Starlink without launch is a generic satellite ISP. xAI without COLOSSUS is a generic frontier lab with cloud bills. The moat is the integrated stack, not any single layer.

- Vertical integration is now a marketplace position, not just a cost-control mechanism. The Anthropic contract is a $45 billion validation that integrated AI infrastructure can be rented to competing frontier labs. The same logic will apply to launch (already does with NSSL), connectivity (already does with maritime and aviation), and eventually orbital compute (post-2028).

- Governance optimized for compounding looks different from governance optimized for short-term shareholder returns. Whether the discount investors apply to founder-controlled supervoting structures is correct depends on whether the institutional capability to execute outlasts founder dependency. The S-1 is honest that this is unproven.

- The addressable market the company is targeting has no comparable precedent. A $28.5 trillion TAM that includes asteroid mining, lunar manufacturing, and Mars cargo transport is not a marketing claim — it is a regulatory disclosure filed with the SEC. The filing uses the phrase "only company" four times. No incumbent — Blue Origin, ULA, Rocket Lab, Amazon Kuiper, the Chinese state launch program — is positioned at the integrated stack level the S-1 describes. The question for investors is not whether SpaceX's competitive position is overstated. The question is whether the technological gating dependencies (Starship reusability, in-orbit refueling, AI compute satellites, lunar mass driver) close on a timeline that the capital markets can underwrite.

At Digital4.Ai, we call the underlying discipline execution velocity: the ability to build operational systems that compound density and reduce marginal cost per outcome as they scale. The S-1 is a $1 trillion-plus case study in why that discipline matters when applied to physical infrastructure. The same logic governs how we build AI-driven operational systems for our customers — at a smaller scale, with a similar geometry.

The IPO will price governance risk, AI losses, and Starship uncertainty into the valuation. What it will not price — because public markets do not yet have a category for it — is the industrial AI execution capability that makes all three risks worth taking. That is the real story of the S-1. Read it that way.

Sources and Method

This article is based on direct review of the public SpaceX Form S-1, filed with the U.S. Securities and Exchange Commission on May 20, 2026, file number 333-296070, accession number 0001628280-26-036936. The filing is available on SEC EDGAR at sec.gov/Archives/edgar/data/1181412/000162828026036936/spaceexplorationtechnologi.htm.

All financial figures, operational statistics, capital-structure terms, executive compensation details, and risk-factor quotations are taken directly from the filing. Page references throughout the article correspond to the prospectus page numbers in the registration statement.

The S-1 is the initial registration statement. The price range, share count, and underwriting syndicate will be disclosed in subsequent amendments (S-1/A filings) closer to the road-show. As of publication, the pricing amendment had not been filed.

SEC EDGAR access for this research used the declared user agent Digital4.Ai-Research/1.0 [email protected] (editorial fact-checking for technology journalism) in compliance with the SEC's equitable-access policy.

No price targets, valuation calls, or investment recommendations are offered. This is editorial commentary, not investment research.

This is Article 3 in the SpaceX IPO content sequence. Read Article 1: Colossus Is Not a Data Center Story and Article 2: Starship and Colossus Are the Same Story.