Colossus Is Not a Data Center Story. It Is an Execution Velocity Story.

By David Gassier — April 30, 2026 — 14 min read

Colossus Is Not a Data Center Story. It Is an Execution Velocity Story.

Published: April 2026 | Reading time: 12 minutes

TL;DR: The Anthropic–SpaceX compute deal has been treated as a valuation puzzle for xAI. Reuters Breakingviews called it an "ugly hybrid" — too expensive to be valued like a CoreWeave-style middleman, not yet convincing enough to be valued like a frontier AI lab. That critique is fair. But it misses the deeper signal. The most important thing about Colossus is not whether Grok beats Claude this month. The most important thing is that SpaceX/xAI built one of the largest AI compute infrastructures on Earth at industrial speed — and Anthropic, one of the most advanced AI companies in the world, now wants to use it. The next AI moat may not be model quality. It may be the ability to industrialize intelligence faster than anyone else.

The Deal That Confused Wall Street

On May 6, 2026, at Anthropic's developer conference in San Francisco, head of product Ami Vora announced that Anthropic had signed a partnership giving it access to the full compute capacity of SpaceX's Colossus 1 supercomputer in Memphis, Tennessee. According to the company's own announcement, the deal adds "more than 300 MegaWatts of new capacity" to Anthropic's compute footprint — equivalent to over 220,000 NVIDIA GPUs coming online for Claude within the month.

That number is not a typo. 220,000 GPUs. 300 MegaWatts. One agreement.

For context: that is more raw compute than most national AI programs. It is enough to roughly double Anthropic's serving capacity for Claude Pro and Claude Max users overnight. And in the same announcement, Anthropic confirmed it had also "expressed interest in partnering with SpaceX to develop multiple gigawatts of orbital AI compute capacity" — meaning data centers in space, powered by the sun, cooled by the void.

This is not a normal supplier announcement.

It is one AI lab paying another AI company's industrial arm for capacity that the buyer cannot — yet — build for itself.

The day after the announcement, Reuters Breakingviews published a sharp dissent. Robert Cyran wrote that the deal "clouds SpaceX's AI value." The argument: Elon Musk's xAI, valued at $250 billion in its February 2026 merger with SpaceX, "owns second-tier social network X and trains behind-the-curve language models." If xAI is renting out Colossus to a competitor, perhaps it is not compute-constrained — and perhaps it deserves the multiples of a CoreWeave-style infrastructure middleman, not those of a frontier AI lab.

In the same week, Blue Owl marked up its SpaceX stake by 36% to roughly $526 per share, after previously selling about half its stake at a $1.25 trillion valuation — a 10× return on the realized portion. The market is voting that something about SpaceX is enormously valuable. The disagreement is about what.

That disagreement is exactly where the interesting story lives.

Reuters Has a Point — And Then Misses One

The Breakingviews critique deserves a fair hearing. It contains three honest observations.

First, xAI is not capacity-constrained if it is willing to give Anthropic the entirety of Colossus 1. A model lab racing to the frontier hoards compute. It does not lease its biggest cluster.

Second, Grok is not yet at the frontier. Whatever you think of its style or its moderation philosophy, the published benchmarks still trail Anthropic's, OpenAI's, and Google's flagship models on most reasoning tasks.

Third, the valuation framing is genuinely awkward. A CoreWeave or a Nebius gets revenue-multiple discipline. A frontier lab — OpenAI, Anthropic, Google DeepMind — gets thesis-driven multiples on optionality. xAI is being asked to be both at once.

All three points are correct. But all three points share an assumption: the most valuable AI company is the one with the best chatbot.

That assumption is from 2023.

In 2026, the binding constraint on AI is no longer model architecture. It is electricity, real estate, GPU allocation, networking fabric, cooling capacity, and the operational ability to compose all of those into something useful, on a deadline. Anthropic itself just admitted as much. If a frontier lab with $61 billion in funding cannot build its own 300 MW supercomputer fast enough to meet user demand, then "having the best model" is no longer the only — or even the primary — moat in AI.

The better question is the one Reuters did not ask:

What if the next AI moat is not model quality, but the ability to industrialize AI infrastructure faster than anyone else?

Colossus Is an Execution Artifact

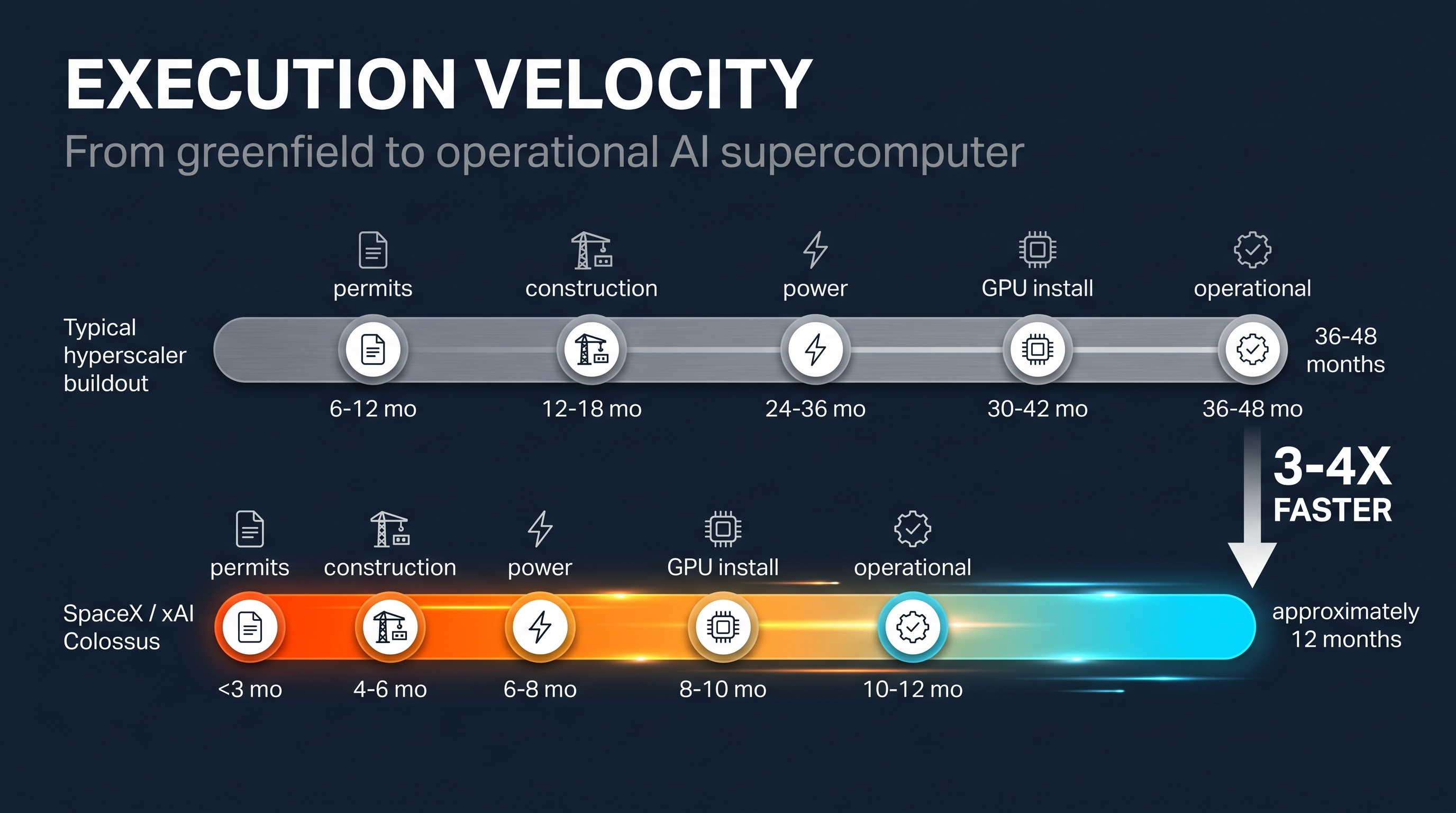

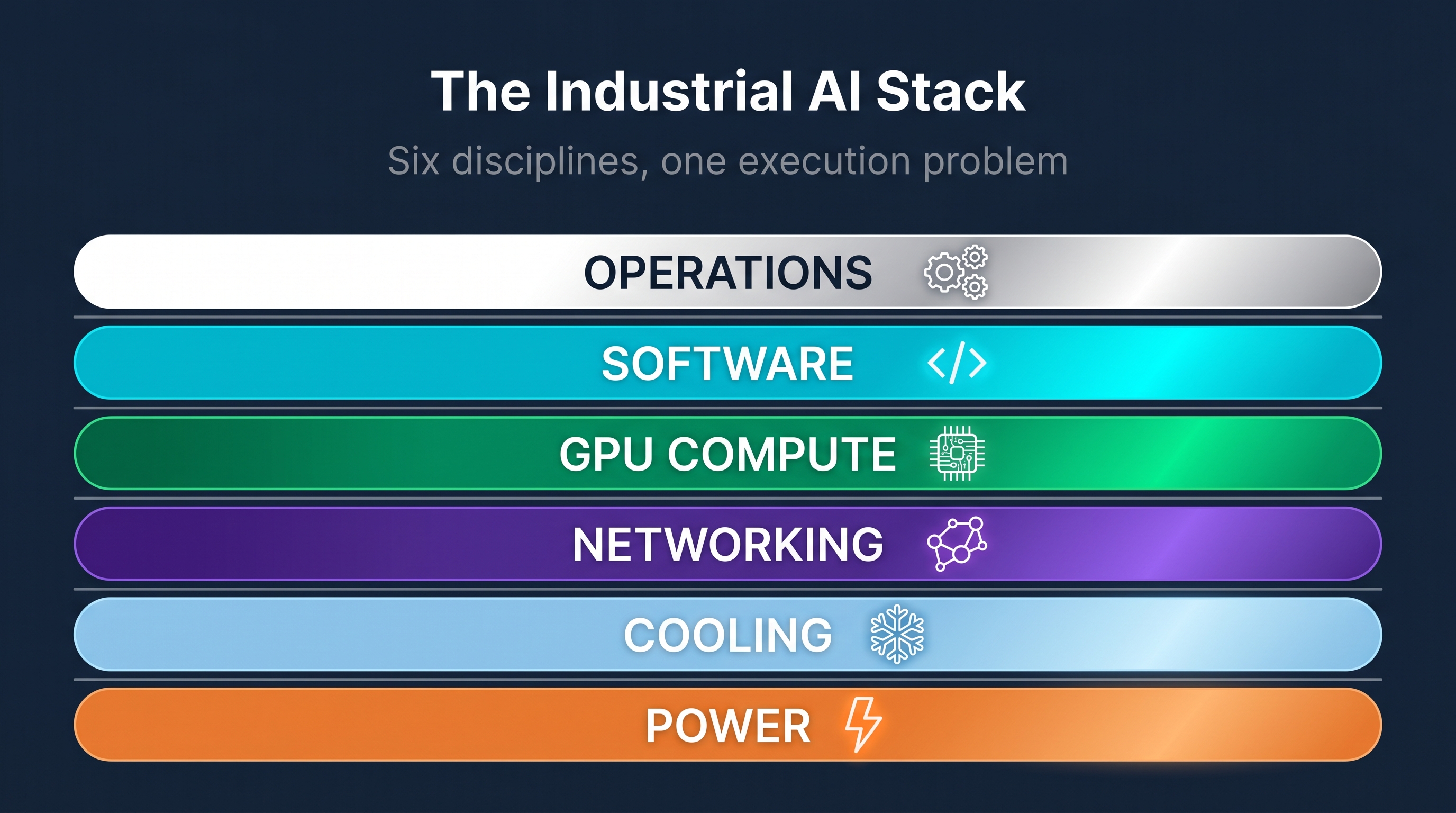

To understand why this matters, look at Colossus 1 not as a building, but as a proof of execution capability.

Colossus is not a single thing. It is a stack of disciplines that almost no organization on Earth can compose simultaneously, in time, at scale.

To bring 220,000 GPUs online in roughly twelve months — a timeline that became public when xAI announced Colossus 1 in late 2024 and operationalized it through 2025 — you need to do all of the following in parallel, not serially:

- Site selection and permits (often 6–12 months alone)

- Substation acquisition and 300 MW interconnect (the slowest step in most data center builds; often 24+ months)

- Building shell + cooling infrastructure (custom water + air systems sized for 700 watts per chip)

- Networking fabric (InfiniBand or equivalent at 220K-port scale, plus the optics, plus the physical cabling)

- GPU procurement (220,000 H100s/H200s in a single allocation is not a phone call you make to NVIDIA — it is a year-long negotiation involving everyone above CEO)

- Logistics (each of those GPUs is a fragile, $30-40K piece of hardware shipped from Taiwan, staged, racked, and tested)

- Software stack (cluster scheduler, distributed training framework, observability, security)

- Operations (24/7 uptime engineering, security, supply chain for replacements at the scale where statistical failures become daily events)

- Capital allocation (~$5–8 billion in CAPEX, deployed against a single thesis, on a hard deadline)

Most companies cannot do any one of these things at speed. SpaceX/xAI did all of them in parallel.

The most important thing about Colossus is not that it exists. It is how quickly it became operational at a scale that matters.

That is not a software achievement. It is an industrial one. And industrial achievements are the kind that compound — because once you have done it once, you can do it again. (Colossus 2 is already under construction.)

SpaceX DNA Entered AI

The reason SpaceX/xAI could do this is that SpaceX is, structurally, an industrial execution machine that learned how to do impossibly hard physical things on aggressive timelines. That muscle did not appear by accident. It was built over twenty years of solving problems that almost everyone said were too hard:

- Reusable rockets — declared impossible by every major aerospace firm before SpaceX did it

- Launch cadence — SpaceX now launches more mass to orbit per year than the rest of the world combined

- Crew Dragon — first commercial crewed orbital vehicle, certified by NASA

- Starlink — the largest satellite constellation in history, deployed in five years

- Starship — the most powerful rocket ever built. On May 7, 2026, the same week as the Anthropic deal, SpaceX completed a full-duration, full-thrust 33-engine static fire of the Starship V3 Super Heavy booster

The cultural ingredients are well-documented at this point: rapid iteration, extreme ownership, vertical integration, manufacturing mindset, willingness to solve ugly physical problems, and relentless schedule pressure. People debate whether that culture is reproducible. It is not. That is the moat.

What is new is the realization that AI infrastructure is now a physical-world manufacturing problem. Not a software problem with a hardware tail — a manufacturing, power, supply chain, civil engineering, and systems integration problem first, with software on top.

That reframing changes who is plausibly positioned to win. The companies best at industrializing physical systems on aggressive timelines are now relevant — sometimes more relevant — than the companies best at training transformer models.

SpaceX has spent two decades training that exact muscle. Now it is being applied to AI infrastructure.

That is the signal underneath Colossus.

Anthropic Validates the Infrastructure

Step back from the valuation debate for a moment and look at what Anthropic just did.

Anthropic is not a fragile or naive buyer. It is one of the most technically sophisticated AI organizations in the world, backed by Google and Amazon, with deep operational expertise and the ability to scrutinize compute providers with a level of rigor most enterprises cannot match. Anthropic does its diligence. It worries — publicly and loudly — about safety, alignment, governance, and infrastructure quality.

If Anthropic is willing to put all of Claude Pro and Claude Max's incremental capacity on Colossus 1, that means three things:

- The infrastructure is real. It is not a marketing demo or a benchmark cluster. It is production-grade compute that can serve mission-critical workloads at scale.

- The operational layer works. Uptime, networking, cooling, and security are at a level that Anthropic — Anthropic — is willing to bet its user experience on.

- Demand for compute is structurally extreme. Even after $61B+ in funding and Google/Amazon partnerships, Anthropic still cannot build infrastructure fast enough to meet demand. So it leases.

The Anthropic deal may complicate xAI's model-company valuation. But it validates Colossus as real infrastructure for the elite tier of AI.

That is the nuance the Breakingviews piece misses. The deal is simultaneously bad news for the "xAI as frontier lab" thesis and excellent news for the "SpaceX/xAI as industrial AI platform" thesis. It validates the harder, more durable capability.

Maybe xAI Is Not Just a Chatbot Company

This brings us to the speculative-but-strategically-important question: what is xAI actually for?

The conventional read is that xAI exists to build Grok and compete with OpenAI, Anthropic, and Google in the chatbot market. The Anthropic deal makes that read less convincing. If you are racing to the AI frontier, you do not lease your biggest cluster to a competitor.

There is a different read. It is speculative and should be labeled as such. But it fits the available evidence better.

SpaceX faces an extraordinary set of operational problems that almost no other organization on Earth is dealing with at scale:

- Autonomy at planetary scale — Starlink's 7,000+ satellites coordinating, deconflicting, and routing traffic in real time

- Logistics across multiple physical environments — factories, launch pads, recovery vessels, downrange sites, customer terminals

- Manufacturing optimization — Raptor engines, Starlink terminals, Dragon capsules, all built at unprecedented cadence

- Simulation and systems modeling — every launch is a simulated rehearsal first

- Closed-loop physical systems — recovery, re-flight, fuel cycle management, lunar/Martian planning

- Engineering acceleration — turning months of design cycles into weeks

This is a class of problem where a sufficiently large AI infrastructure becomes a strategic weapon. Not as a chatbot. As an internal coordination layer. As a simulation substrate. As an autonomy backbone.

There is no public evidence that Colossus is being used for Mars terraforming or planetary logistics. That is not the claim. The claim is more measured:

The class of problems SpaceX faces — autonomy, logistics, simulation, resource allocation, closed-loop industrial systems — is exactly the class of problem where large-scale AI infrastructure becomes strategically valuable. And SpaceX has visible, repeated, hard-won expertise in solving those problems.

If that read is correct, xAI is not primarily a chatbot bet. It is an industrial intelligence bet, with Grok as the consumer-facing surface and Colossus as the deeper asset.

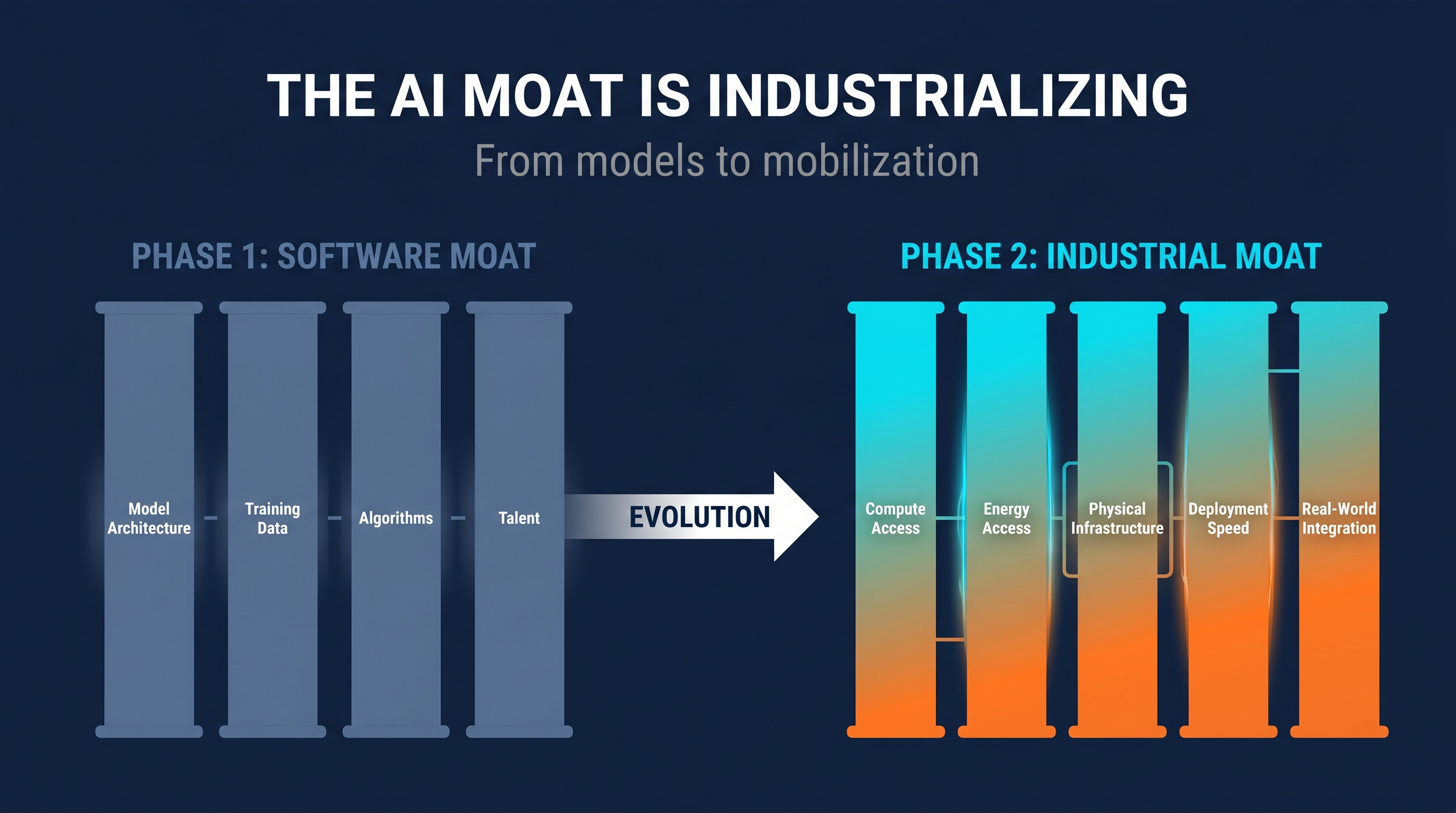

The Real AI Moat May Be Industrial

Zoom all the way out. Phase 1 of the AI race — call it 2017 to 2024 — rewarded a specific stack of capabilities: model architecture, training data, algorithmic talent, and access to whatever compute you could find.

Phase 2 looks different. Phase 2 is industrial.

In Phase 2, the constraints binding AI progress are physical: gigawatt-scale electricity, transmission lines, water for cooling, advanced packaging at TSMC, networking optics, multi-billion-dollar facilities, and the operational discipline to actually build and run them. None of those are software problems. All of them are problems where the right cultural DNA is industrial — manufacturing, supply chain, civil engineering, systems integration — not academic.

This is why traditional hyperscalers (Microsoft, Amazon, Google, Meta) are increasingly partnering with utilities, nuclear operators, and even rocket companies. It is why $630 billion of hyperscaler AI capex projected for 2026 is now bottlenecked by permits, transformers, and grid interconnects — not by chips. It is why an AI lab leasing capacity from a rocket company is not a paradox. It is the new normal.

The next AI race may look less like a software competition and more like an industrial mobilization.

The companies that win Phase 2 may not be the ones with the best model. They may be the ones that can build, power, cool, network, deploy, and operate AI infrastructure at wartime speed. That is a profile that includes SpaceX/xAI. It also includes a small number of others: Microsoft (with Azure + nuclear PPAs), Google (with TPU vertical integration), and a handful of energy-rich nation-states.

Most pure-play AI labs are not on that list.

What This Means for Business Leaders

If you are running a business that is not building 300 MW supercomputers — which is to say, virtually every business — there is still a useful lesson buried in all of this. The lesson is not "build a Colossus." The lesson is about how AI advantage actually accrues to the operating layer.

Most companies treat AI as a chatbot to bolt onto a workflow. They license a model, drop in a prompt, and call it a transformation. That is the 2023 mindset. It is no longer enough.

The deeper lesson from Colossus is that AI value comes from integration, not bolt-on. SpaceX did not buy a chatbot. It built infrastructure that becomes part of how the company actually operates — engineering, logistics, manufacturing, autonomy. The same principle scales down. For an SMB, "AI advantage" does not look like a smarter chatbot on the website. It looks like:

- An AI agent that owns customer email triage end-to-end

- A knowledge layer that remembers every conversation, document, and decision

- A scheduling intelligence that integrates with calendars, channels, and CRM

- An operational dashboard that surfaces what matters before you ask

- A communication layer that acts with proper guardrails, not just responds

That is the operating-system frame. Models are commodities. Infrastructure is becoming the moat at the high end. And at the SMB end, the moat is operational integration — turning AI from a clever conversation partner into an embedded employee with memory, channels, security, and accountability.

The companies that win in their markets — at any scale — will be the ones that figure that out fastest.

Conclusion: The Industrial Era of AI

The market is asking whether SpaceX is a rocket company, a satellite company, an AI company, or an infrastructure company. The Anthropic deal exposed that the question itself may be wrong.

Maybe the better answer is:

SpaceX is becoming an industrial execution platform. And Colossus may be the clearest evidence yet of what that platform can do when pointed at AI.

Reuters is right that the deal complicates xAI's valuation. It is awkward as a model-lab story. But the awkwardness is the signal, not the noise. The Anthropic deal is messy precisely because it does not fit the old categories — "frontier lab" vs. "compute middleman." It fits a new category that the market has not yet priced: industrial intelligence platform.

The breakthrough was not Grok.

The breakthrough was Colossus.

And Colossus is just the beginning.

A Note for Operators

If you have read this far, here is the takeaway worth keeping. You will not build a Colossus. You do not need to. But the lesson underneath it — that AI value comes from integration, not bolt-on, and that the operational discipline matters more than the model choice — applies at every scale. The companies that win their markets in the next five years will be the ones that figure out where AI fits as an operating layer, not as a feature.

That is the work we do at Digital4.ai. The CTA below leads to the most useful version of that conversation.

Sources & References

- Anthropic. Higher usage limits for Claude and a compute deal with SpaceX — May 6, 2026

- Reuters Breakingviews. Anthropic deal clouds SpaceX's AI value — May 7, 2026

- Reuters. Blue Owl marks up SpaceX stake by 36% to around $526 per share — May 7, 2026

- Reuters. Blue Owl sold about half its SpaceX holding at $1.25 trillion valuation — April 30, 2026

- Space.com. SpaceX just fired up its 33-engine Starship 'V3' Super Heavy rocket booster — May 7, 2026

- Storage Review. Anthropic Signs SpaceX Colossus 1 Deal For Major Claude Compute Expansion — May 2026

- Reuters Breakingviews. How Big Tech's $630 bln AI splurge will fall short — March 26, 2026

David Gassier is CEO and Chief Technology Officer of Digital4.ai. He writes about the operational side of AI — where it actually creates leverage in real businesses, and where it does not.